To qualify for the Innovation Tax Credit (ITC), which is an extension of the Research Tax Credit (RTC), your company and your projects must meet certain conditions.

However, this scheme can be used for expenditure incurred up to December 31, 2027.

So how do you go about it?

At Kairos, we have valid Innovation Tax Credit approval, so we can help you with your project.

Here's the complete checklist of actions you need to take to qualify for this scheme.

Crédit d'Impôt Innovation (CII): the eligibility checklist.

To qualify for the Innovation Tax Credit (ITC), which is an extension of the Research Tax Credit (RTC), your company and your projects must meet certain conditions.

However, this scheme can be used for expenditure incurred up to December 31, 2027.

So how do you go about it?

At Kairos, we have valid Innovation Tax Credit approval, so we can help you with your project.

Here's the complete checklist of actions you need to take to qualify for this scheme.

1. Your company's eligibility criteria.

a) SME status

Your company must meet the EU definition of a small or medium-sized enterprise (SME).

b) Number of employees

Less than 250 employees.

c) Annual sales

Not exceeding 50 million euros OR an annual balance sheet total not exceeding 43 million euros.

These thresholds are determined by the type of shareholding (affiliated, partner or independent company).

d) Tax system

The company must be subject to a real (normal or simplified) corporate tax (IS) or income tax (IR) regime.

e) Tax-exempt companies

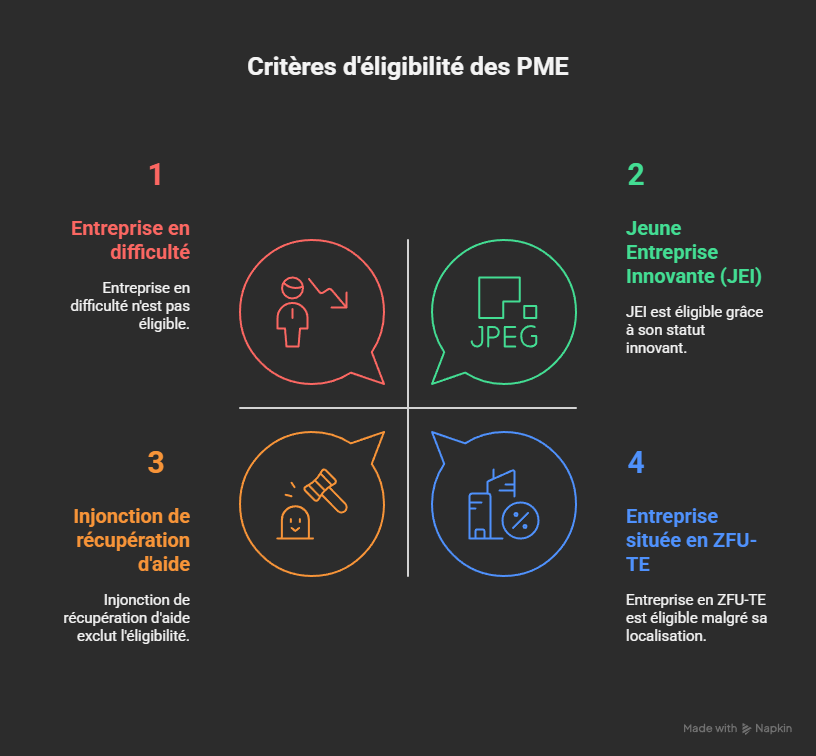

The scheme also applies to certain temporarily tax-exempt companies, if they fall into one of the following categories:

Young Innovative Company (JEI).

Company created to take over a company in difficulty.

Companies located in specific zones: Zone d'Aide à Finalité Régionale (AFR), Zone Franche-Urbaine / Territoire Entrepreneur (ZFU-TE), Bassin d'Emploi à Redynamiser (BER), Zone de Restructuration de la Défense (ZRD), Zone Franche d'Activité des départements d'Outre-mer, Zone de Revitalisation Rurale (ZRR), Bassin Urbain à Dynamiser (BUD) and Zone de Développement Prioritaire (ZDP).

f) Exclusions for companies

Not eligible for the CII :

Companies subject to an outstanding recovery order.

Companies in difficulty, unless they were not in difficulty on December 31, 2019 and became so between January 1, 2020 and December 31, 2021.

2. Eligibility criteria for your innovation project.

a) Nature of operations

The ITC applies specifically to projects involving the design of prototypes or pilot plants for "new products".

A "prototype" is an original model possessing the technical qualities and operating characteristics of the new product, even without its final appearance.

It must not be intended for the market, but as a model for a new product.

b) Definition of "new product

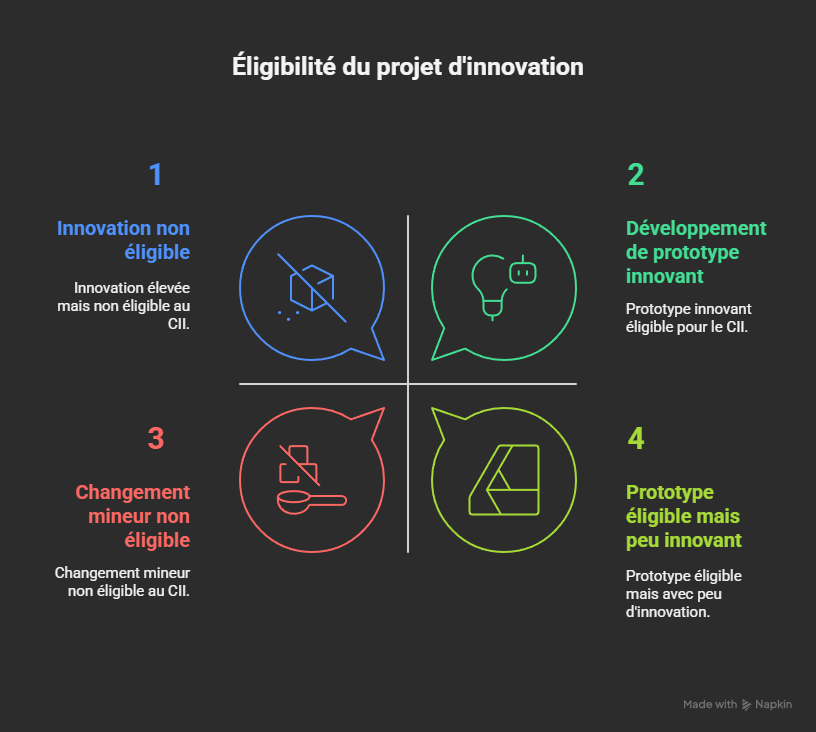

To be eligible, a product must satisfy two cumulative conditions:

It must not yet have been made available on the market.

It must stand out from existing or previous products through superior performance in terms of technology, eco-design, ergonomics or functionality.

Simple changes in a product's appearance or minor evolutions are not sufficient for eligibility.

c) Eligible phases

Only expenditure from design to prototype or pilot installation of a new product is eligible for the CII.

The phases of defining specifications, mock-up, design (POC, product), production and testing of prototypes are all worthwhile.

d) Service innovations

If they are based on innovative software or products, they may be eligible.

e) Project exclusions

Expenses relating to the production phase of the prototype or pilot plant for the new product are not eligible.

Marketing and sales expenses are not covered.

3. Eligibility criteria for your expenses.

Expenses eligible for the CII are defined in k of II of article 244 quater B of the CGI.

They cannot be added to those already taken into account in the CIR base for the same operation.

Public subsidies received for innovation projects must be deducted from the amount of expenditure taken into account when calculating the ITC.

a) Depreciation and amortization

Only depreciation allowances for assets or buildings created or acquired as new and directly assigned to the design of prototypes or pilot plants for new products are eligible.

In the case of mixed use (innovation-non-innovation), depreciation is taken pro rata to the actual time of use for design operations.

b) Personnel expenses

Remuneration and related costs, as well as compulsory social security contributions, for personnel directly and exclusively assigned to the design of prototypes or pilot plants for new products.

Support staff are expressly excluded.

Remuneration for part-time staff or staff assigned during the year is taken into account on a pro rata basis according to the time actually devoted to these operations, excluding any lump-sum calculation.

More varied profiles than for the CIR (engineers, PhDs) are accepted, including developers or designers.

Personnel costs do not require a specific level of qualification for eligibility, the focus being on the innovation activity itself.

c) Outsourced expenses (subcontracting)

Expenditure on third-party design of prototypes or pilot plants for new products.

The service provider must have Innovation Tax Credit approval.

Approval is granted by the Minister for Industry, unless the company is already CIR-approved, in which case it is granted by the Minister for Research.

You must check the validity of the approval and request the official certificate.

The work carried out by the service provider must be eligible for the ITC (for example, market research, training and marketing are not covered).

A contract specifying the innovation activities, invoices and related documentation are required.

If the ordering company is not eligible for the CII (for example, because it does not meet the conditions set out in k of II of Article 244 quater B of the CGI), the approved company that carried out the operations can take the corresponding expenses into account when calculating its own CII.

d) Intellectual property expenses

Amortization, patent and plant variety certificate (PVC) acquisition and maintenance costs.

Design registration, maintenance and defense fees.

These costs must relate to the design of prototypes or pilot plants for new products.

Trademark registration fees are not eligible.

Other operating expenses: These expenses are no longer eligible for the ITC if incurred after January 1, 2023.

4. Expenditure limits and rates.

Total eligible expenditure is capped at €400,000 per year.

This ceiling applies only once a year, regardless of the number of prototypes or pilot installations.

The CII rate is 20% of eligible expenditure for expenditure incurred after 2025 (compared with 30% before).

Higher rates apply in Corsica (40% for small businesses, 35% for medium-sized businesses) and the French overseas territories (60%).

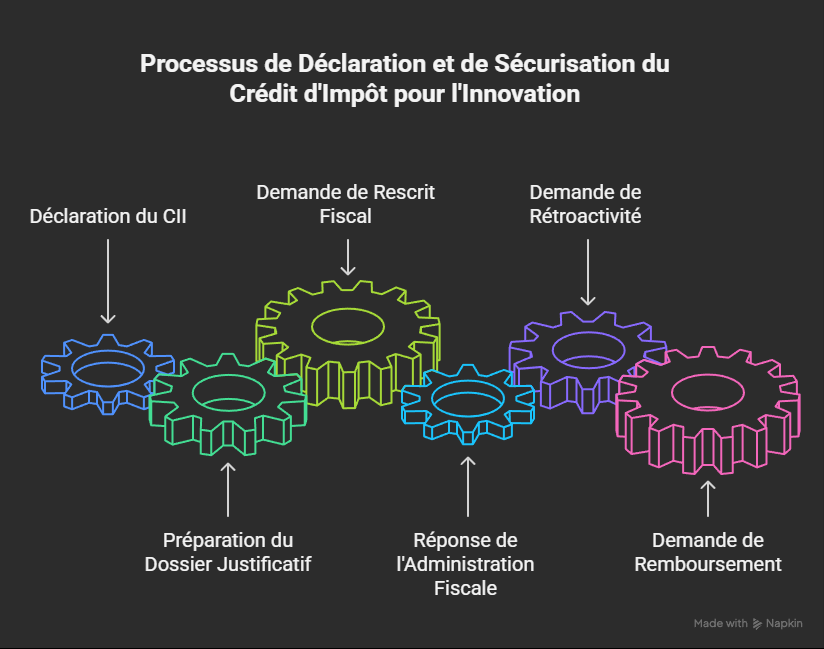

5. The declaration and security process

a) Declaration

The ITC is declared using form no. 2069-A-SD, which must be attached to the income tax return.

Companies subject to corporate income tax must declare their income no later than the 15th of the 4th month following the end of the financial year. For companies with a December 31st year-end, the deadline is May 15th of the following year.

Companies subject to income tax must declare their income no later than 15 days after the 2nd working day following May 1st.

The ITC is calculated for each calendar year (January 1 to December 31), regardless of the year-end.

b) Supporting documentation

A supporting technical file must be drawn up to prove the eligibility of the activities.

It must be supplied on request.

It must describe the work, the state of the competition/market, and the profiles of the personnel involved.

It is advisable to draw it up at the time of declaration, as the administration may request it within 3 years of the declaration.

c) Tax rescript

Companies can seek prior advice from the tax authorities (rescrit fiscal) to ensure the eligibility of their expenses.

The opinion is given by the Minister for Industry or Research.

The application must be submitted no later than six months before the deadline for filing the CIR-CII declaration.

The tax authorities respond within three months; if no response is received, this implies tacit agreement, which can be invoked in the event of a subsequent audit.

This guarantee is only valid if the company's actual situation corresponds precisely to the situation described in the rescript.

Each rescript request must relate to a single project.

d) Retroactivity

It is possible to reclaim the ITC on innovation expenditure incurred over the last three years by means of an amending declaration.

e) Reimbursement

The ITC is deducted from the company's income tax liability.

If the amount of tax is insufficient, the excess can be carried forward to the following 3 years or, for SMEs and certain companies (JEI, new companies or companies in difficulty), be reimbursed immediately.

.jpg)