Is your law firm ready for the e-billing revolution?

Time is of the essence: the reform in France, dictated by the Finance Act, imposes a major digital transition with a strict timetable pointing to September.

This tax obligation to dematerialize invoices affects every business, and the legal profession is no exception.

Between issuing and receiving dematerialized invoices, VAT management, data reporting to the authorities, and the necessary compliance, the stakes are colossal.

Which software solution should you choose for secure transmission that respects professional secrecy while optimizing the processing of each document and service?

This article is your guide to transforming this obligation into a real opportunity to improve your firm's productivity and customer relations.

The dematerialization of invoices is transforming the legal profession.

What are the challenges and concrete changes for your firm beyond compliance?

a) Meeting an unavoidable legal obligation.

1. Understanding the reform of electronic invoicing in France: The framework imposed by the Finance Act.

The reform of electronic invoicing in France is part of a process to digitize the entire economic life of companies.

The legislative framework was set by the amended Finance Act for 2022 (art. 26) and Decree no. 2022-1299 of October 7, 2022.

Article 91 of the Finance Act for 2024, however, modified the initial implementation schedule, postponing the obligation.

2. Anticipate new tax authority requirements: e-invoicing, e-reporting, and data transmission.

The reform involves two main obligations:

Obligatory electronic transmission of domestic invoices exchanged between professionals (e-invoicing).

The obligation to transmit invoicing data for other transactions (international, intra-Community, B2C) (e-reporting).

E-invoicing involves the transmission of invoices in electronic format via a state or private platform, with the involvement of the tax authorities.

E-reporting concerns the transmission of certain information to the tax authorities for transactions not covered by e-invoicing, enabling the reconstruction of a company's economic activity.

This mechanism is specifically designed to combat VAT fraud.

The tax authorities will therefore benefit from a complete and instantaneous view of invoicing information.

La réforme fiscale met désormais l'accent sur la qualité des données et leur exploitation immédiate par l'administration, facilitée par l'intelligence artificielle.

3. Align with European directives and market standards (B2B, public sector via Chorus Pro).

The reform is part of a global and European context.

It has been authorized by a European law and is inspired by directives and regulations such as eIDAS.

The obligation to dematerialize invoices has first affected the public sector since 2017/2019 via the Chorus Pro platform.

It is now gradually being extended to the private sector for transactions between VAT-registered parties (B2B).

Companies can use :

or to the public billing portal (PPF),

or to a certified dematerialization platform (PDP) to exchange invoices and transmit data to the administration.

Specific formats such as Factur-X are required.

b) Modernize internal processes for greater agility.

1. Out with the paper invoice: the limits of manual processing and physical archiving.

The modernization of administrative practices involves the dematerialization of invoices, marking the end of paper-based invoicing.

Electronic invoices can be created, sent and stored more quickly, without the need for large quantities of binders or physical storage space.

Manual processing and paper archiving are time-consuming, error-prone, and less secure and traceable than digital systems.

Dematerialization reduces printing and shipping costs and improves transaction traceability.

2. Meeting the challenges of digitalization: staying competitive in a legal market undergoing digital transformation.

Faced with the new challenges of the legal market, dematerialization is a strategic necessity that goes beyond the simple stage of technological evolution.

The legal sector is becoming increasingly digital, and digitizing law firms is essential to remain competitive.

The rise of legaltech is facilitating this digital transition by automating and optimizing tasks.

Overcoming the challenges of digitization requires optimized procedures and the use of advanced information systems to process the growing volume of data.

3. Optimize the use of resources: reduce time spent on low value-added administrative tasks.

The dematerialization of invoices for law firms represents a time-saving opportunity.

Automating the creation, dispatch and follow-up of invoices reduces manual tasks, allowing the client to concentrate on higher value-added assignments, i.e. the lawyer's core business.

Using the right billing software can automate time-consuming management tasks, freeing up your time.

c) Strengthen customer relations and the firm's image.

Beyond legal imperatives and internal optimization, dematerializing invoices is a powerful lever for improving your customers' perception of your firm and strengthening their trust.

It projects a modern image, while simplifying financial interactions.

1. Offer a smooth, modern payment experience: Simplify the sending and receiving of invoices for your customers.

The modernization of administrative practices through the dematerialization of invoices facilitates management and contributes to smoother data processing.

Electronic invoices can be :

created,

sent

and stored with greater speed.

Dematerialization facilitates exchanges with third parties, making interactions smoother and less prone to manual error.

For the customer, this means simpler sending and receiving of invoices.

What's more, dematerialization facilitates the exchange of information, which can shorten invoice complaint times and speed up collection.

Some e-billing solutions enable customers to pay their invoices directly online by credit card or SEPA direct debit, often via a unique link automatically added to invoices or e-mails.

This online payment option is a modern feature that simplifies life for customers and speeds up the receipt of payments.

Electronic invoicing offers greater reliability, without the hassle of lost mail, and a certified dispatch date.

2. Project an image of professionalism: Show that your firm is at the cutting edge of technology and compliance.

The adoption of electronic invoicing marks the end of the paper era, perceived as time-consuming and error-prone.

By adopting these technologies, firms demonstrate that they are at the cutting edge of technology and ready to meet the challenges of digitalization.

The use of appropriate billing software ensures compliance with legal standards and data security, thus projecting an image of professionalism.

Dematerialization also contributes to an eco-responsible approach by reducing printing and shipping costs, which is beneficial for the image of firms with customers who are increasingly sensitive to sustainable practices.

Early compliance reassures important customers.

3. Improve transparency and customer relations: facilitate access to billing information linked to files.

Electronic invoices offer precise tracking of transactions, for greater transparency.

Clear, accessible financial documents strengthen relations between companies.

Transparent invoices that show :

details of the due diligence performed,

applied hourly rates

or the time consumed by a package,

help maintain a relationship of trustbetween lawyer and client.

The clarity and transparency of our invoices, as well as the results obtained and the quality of our customer relations, contribute to customer loyalty.

Customers expect to be billed at a level they feel is fair, in line with the work and value received.

Dematerialization also means that customers can easily find their invoices without having to contact the secretariat.

Some software packages enable customers to instantly view all the elements linked to their file, including paid and unpaid invoices.

2) How do I implement electronic invoicing?

The stakes are clear, the need is there.

But where to start?

Implementing electronic invoicing can seem like a mountain.

However, with a structured approach, this transition can be made very smoothly.

The aim is to ensure a smooth transition to this technology.

So what are the key steps for a successful implementation, without disrupting your core business?

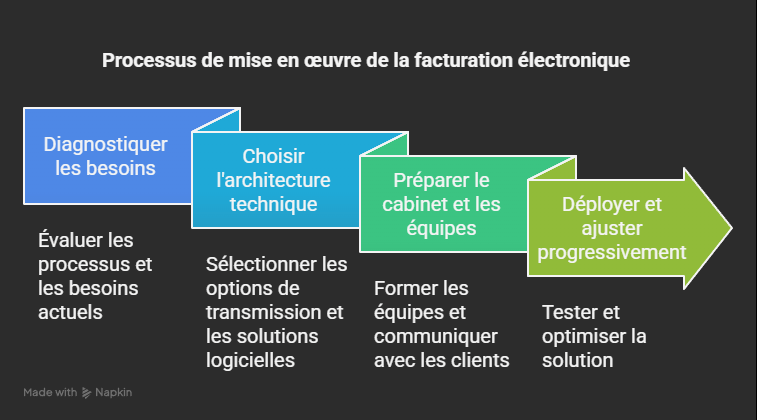

a) Diagnose your current needs and processes.

To make a successful transition to electronic invoicing, you need to start by assessing your existing organization.

1. Analyze the volume and nature of your invoices (fees, services, B2B/B2C customers).

In your legal practice, billing concerns services and fees.

The themes of dematerialization and electronic evidence are of interest to the private sector:

companies,

legal entities,

private individuals

and the public sector:

administrations,

communities,

public institutions.

The dematerialization of invoices has applied to the public sector since a 2019 law and is gradually being extended to the private sector.

The electronic invoicing obligation applies to domestic transactions between VAT taxpayers.

2. Map your existing invoicing circuit: from invoice creation to archiving, validation and payment.

Today, invoicing can involve many time-consuming tasks.

Some firms still use "old-fashioned" methods such as invoicing in Word or Excel, which can be a source of errors and management headaches.

The billing process includes :

creation,

the shipment,

treatment,

follow-up,

payment,

and invoice archiving.

You need to identify your current invoicing processes to assess how e-billing can be integrated into your existing tools.

Electronic invoice management is designed to improve traceability and security.

3. Evaluate your current hardware and software (practice management, accounting).

Invoicing software adapted to lawyers is recommended.

There are practice management software packages that integrate electronic invoicing, as well as dedicated solutions.

To ensure operational continuity, you need to assess your IT assets and check that your current tools are compliant.

Today's electronic invoicing systems guarantee rigorous data protection.

It is imperative to give absolute priority to the security of information transmitted.

Some software packages offer data centralization functions.

Integrated platforms can centralize all your contacts and documents.

The security of your customers' and your firm's data must be protected by advanced encryption systems and security protocols.

b) Choose the right technical architecture.

Switching to electronic invoicing involves more than just changing software: it also means choosing the right technical architecture for your practice.

1. Understanding transmission options: Partner Dematerialization Platform (PDP) vs Public Billing Portal (PPF) - which model for your practice?

The electronic invoicing system provides two transmission models based on a "Y" system.

Companies can use :

or directly to the Public Billing Portal (PPF) ,

or to a certified Partner Dematerialization Platform (PDP).

The PPF is a shared portal provided free of charge by the French government.

A PDP is a certified private platform.

The transmission model is based on the Chorus Pro portal used for public procurement.

The "Y" system is based on a public platform that centralizes billing information for the tax authorities.

The data reaches him:

or directly via the public platform,

or via certified private platforms, which transmit the invoice to the customer and communicate the data to the centralizing public platform.

The tax authorities will have an overview at all times.

2. Selecting the right software solution: do you need dedicated software or an integrated platform? What criteria should be selected?

Find e-invoicing platforms that comply with regulations.

Law firms have specific billing management needs.

Good invoicing software frees you from this time-consuming task.

Solutions such as those proposed by :

Docaposte,

Axonaut,

Tempolia,

Tiime,

Hub Avocat

or SECIB Neo,

are designed to meet the stringent compliance and safety requirements of the legal sector.

The chosen solution must include electronic signature and digital archiving.

Some software packages, such as Axonaut or Hub Avocat, are presented as all-in-one tools, applications or integrated platforms.

The use of SaaS billing software for lawyers is highly recommended.

Electronic signatures are based on a qualified certificate created by a secure device, often issued by a certification service provider.

3. Anticipate interconnection with your existing systems: Ensure data flow between tools.

You need to assess how to integrate e-billing into your existing tools to maintain operational continuity.

Software that complies with the new regulations offers many advantages for centralizing all data.

The aim is for dematerialized invoices to be integrated directly into companies' accounting software.

Information exchange with third parties, such as accountants, is facilitated.

The transfer of financial information becomes almost immediate, and accounting management is more precise and responsive.

EDM (Electronic Document Management) solutions for law firms are designed to :

centralize,

organize

and exploit documents,

including invoices, and can interconnect with other modules to process incoming invoices.

c) Prepare your practice and your teams.

Once the requirements have been identified and the technical architecture chosen, the success of the transition depends on the preparation of the whole firm.

1. Define a clear transition plan: timetable, resources, responsibilities.

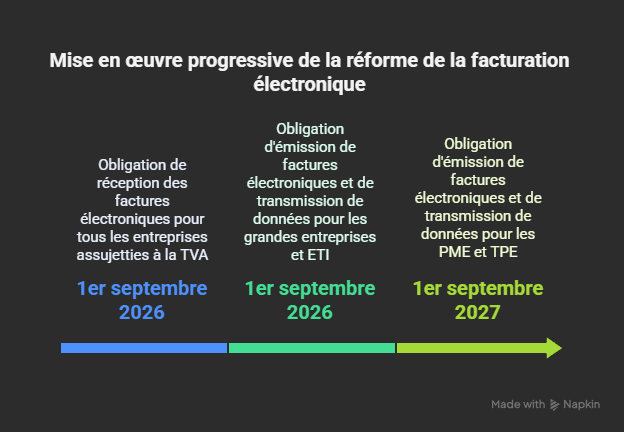

The reform of electronic invoicing, initially planned on a progressive timetable, has been postponed.

The new timetable provides for a staggered entry into force, starting on :

September 1, 2026 for large companies and ETIs,

and September 1, 2027 for SMEs and micro-businesses in the process of being transferred.

The acceptance requirement will apply to all companies from September 1, 2026.

You need to prepare for this in advance, rather than a few months in advance.

Setting up the system requires an inventory of the existing system (flows, processes, tools, data) and an impact analysis to define a target model.

We need to anticipate the costs, particularly in terms of IT equipment and training, especially for smaller structures.

2. Support human change: train your staff in new document management tools and processes.

Transition means leaving behind the "old way" of doing things.

You need to train your teams and make them aware of the challenges of electronic invoicing and how to use the new tools.

Lexing's Dematerialization business unit provides training on these subjects.

3. Communicate with your customers and suppliers: inform them of the switch to electronic invoicing.

You need to inform your customers of the switch to electronic invoicing and obtain their agreement.

Explain the benefits in terms of :

safety,

efficiency

and speed.

For corporate customers, their invoices will be made available automatically.

For customers who are not subject to VAT (private individuals, for example), the question arises of how to reconcile the legal obligation to transmit information with respect for professional secrecy.

The Conseil National des Barreaux (CNB) has expressed reservations and suggests that lawyers should only transmit information not covered by secrecy (e-reporting without B2B customer identity).

Other avenues are being explored, such as passing on the details of due diligence separately, or obtaining the customer's agreement to waive professional secrecy in order to meet obligations.

As far as suppliers are concerned, the dematerialization of incoming invoices facilitates their management.

d) Deploy and adjust gradually.

For a successful transition, gradual deployment and ongoing monitoring are recommended.

1. Launch a pilot phase: Test the solution on a restricted perimeter (specific files or customers).

The Administration has launched a pilot phase to test the system ahead of general deployment.

Companies will be able to practice exchanging electronic invoices via PPF and PDP.

It's a good idea for a firm to consider an internal test phase on a limited perimeter before generalizing the use of a solution.

2. Gather feedback and optimize : Adjust settings and processes before general deployment.

The pilot phase is an opportunity to finalize the IT development of the solutions and guarantee data security and confidentiality.

Internally, testing on a restricted perimeter allows you to :

gather feedback from users,

identify blocking points

and adjust settings or processes before widespread deployment.

Scalable applications such as Tiime or Hub Avocat incorporate user feedback to drive improvements.

3. Provide post-implementation support: maintenance and guidance.

After implementation, support and maintenance are required.

Support teams are available to help users.

Software solutions are frequently updated to keep pace with changing needs and regulations.

Professional support can include :

needs audit,

compliance audit,

set-up assistance

and training.

3) What are the tax obligations for lawyers?

The reform is not just a recommendation, it's a legalobligation with specific tax implications.

For lawyers, as guarantors of the law, compliance is essential.

What exactly are the new rules imposed by the tax authorities?

Are you sure you understand what is expected of your firm?

The aim of this reform is to combat VAT fraud and simplify reporting obligations by enabling pre-filling of returns.

This reform is part of a global and European context, inspired by texts such as the European eIDAS regulation on electronic identification and trust services.

Initially scheduled for 2024 and 2026, the entry into force of the e-invoicing obligation has been postponed by the Finance Act for 2024 .

The new timetable provides for a gradual phasing-in from September 1, 2026.

a) The obligation to issue invoices in electronic format (e-invoicing).

This obligation is an integral part of the electronic invoicing reform.

1. Transactions concerned: Focus on domestic B2B operations.

The obligation to issue electronic invoices, known as e-invoicing, mainly concerns domestic transactions between entities subject to VAT in France.

Lawyers, as VAT-registered businesses, are therefore affected.

2. Accepted formats: Factur-X, UBL, CII - goodbye to simple PDF for B2B issues!

For an invoice to be considered "dematerialized" or electronic within the meaning of the law, the entire process - from issue to receipt and archiving - must be electronic, using a specific electronic format.

A simple scan of a paper invoice sent by email in PDF format does not constitute an electronic invoice within the meaning of the law, nor does an invoice created electronically but sent in paper format.

Formats accepted by the tax authorities :

the Factur-X,

UBL (Universal Business Language),

and CII (Cross Industry Invoice),

and other structured formats.

A simple PDF format is acceptable, with documented continuous checks to ensure a reliable audit chain between the invoice and the justified service.

An electronic invoice must :

guarantee authenticity of origin,

content integrity,

and readability of the file from the moment it is issued and throughout its retention period.

This is often ensured by qualified electronic signatures within the meaning of the eIDAS regulation, or by controls via a reliable audit trail.

3. Mandatory transmission platforms: the central role of PPF and PDP.

Electronic invoices must be transmitted via a national platform based on a model similar to Chorus Pro, or via a dematerialization operator (a certified private platform, also known as Plateforme de Dématérialisation Partenaire - PDP).

The tax authorities will use a so-called "Y" system, where invoicing data is sent to a centralized public platform:

or directly (via the public billing portal - PPF),

or through PDPs.

Companies will be able to choose whether to use the public portal or a third-party platform.

The private platform will route the electronic invoices to the customer's platform and communicate the expected data to the public portal.

b) The obligation to receive invoices in electronic form.

In addition to issuing invoices, the reform also imposes an obligation to receive them.

1. An obligation for all VAT-registered companies in France: prepare for dematerialized reception.

According to the new timetable set out in the Finance Act for 2024, all companies, whatever their size, will have to be able to receive dematerialized invoices from September 1, 2026.

2. The need to adapt your supplier invoice processes.

This obligation to receive invoices means that law firms must be prepared to manage their suppliers' invoices electronically.

You need to assess how to integrate electronic invoicing into your existing tools to maintain operational continuity.

This may involve identifying e-invoicing solutions that comply with regulations.

It is therefore important to adapt supplier invoice processing procedures to ensure smooth management and minimize the risk of errors.

It is also essential to inform the firm's customers about the switch to electronic invoicing and obtain their agreement, explaining the advantages in terms of :

safety,

efficiency

and fast transaction processing.

The postponement of the deadlines offers additional time to better prepare for this major digital transition.

c) The obligation to transmit data to the administration (e-reporting).

In addition to e-invoicing, the reform introduces an e-reporting system.

The purpose of this system is to transmit invoicing and tax data to the authorities, enabling them to reconstruct a company's economic activity.

1. Transactions covered: B2C and B2B international transactions, and payment data.

E-reporting specifically concerns transactions not covered by mandatory B2B domestic e-invoicing.

This includes :

non-domestic operations (international B2B transactions, including intra-Community transactions),

transactions carried out with a person not subject to VAT (B2C - Business to Consumer),

and the transmission of certain payment data.

2. Specific information to be transmitted: amount, VAT rate, payment status.

The data to be transmitted for e-reporting is mainly transaction and payment data.

3. The frequency and mode of transmission of this data via the platforms.

The transmission of e-reporting data takes place after the invoice has been issued, but is described as "near real-time" for international and B2C invoices.

The roll-out of this obligation is based on that of e-invoicing, with progressive deadlines depending on company size, starting on September 1, 2026.

Transmission is also possible via a Partner Dematerialization Platform (PDP) or the Public Billing Portal (PPF).

The platform will transmit transaction data to the tax authorities.

d) Respect for professional secrecy in this new context.

For lawyers, a profession subject to professional secrecy, the application of electronic invoicing raises specific difficulties.

Professional secrecy is public policy, general, absolute and unlimited in time, and enjoys constitutional and conventional protection.

1. How can we reconcile data transmission with customer confidentiality?

Article 2.2 of the National Internal Regulations (RIN) protects the customer's identity and address.

During tax audits, the authorities may not request information on the identity of the customer or the nature of the service provided by non-commercial professions subject to professional secrecy [134, note 20].

Lawyers' accounting and tax obligations take precedence over professional secrecy when it comes to justifying their income, but the exceptions to this secrecy are limited and do not authorize automatic transmission to the tax authorities.

Passing on information to private partner platforms is also considered a breach of professional secrecy when customer and service data is passed on to third parties.

The Conseil National des Barreaux (CNB) has expressed reservations and taken a position on this difficulty.

At its annual general meeting, the CNB demanded that lawyers be subject only to e-reporting, with no transmission of the customer's identity or address, even for companies subject to VAT.

Negotiations have been opened with administrative and tax authorities in order to reduce transmission obligations.

The CNB is also concerned about the risk of cross-referencing data transmitted to the administration for profiling purposes or for targeting tax audits not strictly related to VAT, and is demanding legislative guarantees that no data cross-referencing will give access to information covered by confidentiality.

Avenues for reflection include :

anonymization of sensitive data,

transmission of aggregated data,

specific encryption systems,

or the creation of a sovereign platform dedicated to the profession.

Another suggestion is to transmit the details of the due diligence in a document separate from the invoice.

2. The role of software and platforms in securing exchanges and respecting professional secrecy.

The security of transmitted data is an absolute priority, especially as law firms handle sensitive information.

Modern e-invoicing systems must provide robust protection through advanced encryption measures.

Invoices will be stored in a secure area.

Specialized software for lawyers is designed to meet the stringent compliance and security requirements of the legal sector.

They must include functionalities such as electronic signature and digital archiving to guarantee document integrity and probative value.

However, even with certified platforms (PDP), the issue of professional secrecy remains central.

The CNB is concerned about the transmission of data to private platforms and the risk of secrecy being compromised by the cross-referencing of data at administrative level.

It invites further reflection on a dedicated sovereign platform or the labeling of operators making specific commitments to protect data subject to professional secrecy.

Software must be able to adapt to the specific requirements of lawyers, potentially by allowing the anonymization or dissociation of certain information to ensure ethical compliance.

4) What are the advantages of dematerialization?

While compliance is the initial driver, the benefits of e-invoicing go far beyond that.

Imagine a smoother, faster, more profitable practice...

This is the promise of dematerialization.

Get ready to discover how this transformation can become a powerful performance driver.

a) Significant financial gains.

1. Lower direct costs: less paper, ink, postage, physical archiving.

Electronic invoicing reduces printing and shipping costs.

Less paper also means less need for filing cabinets or physical storage space.

In addition to saving on postage and paper archiving, this approach also helps to minimize the firm's environmental footprint, which can improve its image with customers who are sensitive to sustainable practices.

2. Faster payment times: instant transmission, easier monitoring, direct impact on cash flow.

The dematerialization of invoices facilitates the exchange of information, resulting in shorter claims processing times and faster collection.

This improves firms' cash flow management, giving them faster access to the liquidity they need.

Real-time invoice tracking facilitates reminders and reduces payment times.

Invoicing faster and better, controlling payment times, and setting up automatic reminders systems can radically reduce payment times and collection procedures.

3. Lower processing costs: less manual input, fewer errors.

Dematerialization contributes to smoother, less error-prone data processing.

The switch to electronic invoicing is estimated to reduce administrative costs by at least a factor of three.

Less manual data entry means lower processing costs and fewer billing errors.

b) Increased operational efficiency.

1. Significant time savings for lawyers and support teams:

Free up time for legal advice and customer relations.

Simplified invoicing processes save time.

This allows lawyers to devote more time to :

review of files,

to higher value-added missions,

legal advice or representation.

2. Process automation: Validation, dispatch, reminders, reporting...

Let the machine handle repetitive tasks.

Billing software automates all the time-consuming tasks involved in running a practice.

It makes creating, sending and tracking invoices simple and straightforward.

Automating invoice creation, sending and follow-up considerably reduces manual tasks, especially for recurring invoices.

Features such as direct online bill payment and recurring billing are also available.

3. Simplified administrative and accounting management: rapid access to information, easier reconciliation.

Dematerialization facilitates exchanges with third parties, notably accountants, with whom interactions become more fluid and less prone to manual error.

The transfer of financial information becomes almost immediate, and accounting management is more precise and responsive.

Electronic invoices offer precise tracking of transactions, essential for transparency.

Invoicing software lets you manage invoices according to services, fees and agreements, while ensuring legal compliance and simplifying day-to-day management.

c) Enhanced safety and traceability.

The dematerialization of invoices and legal documents provides guarantees in terms of security and tracking, essential for a profession handling sensitive information.

1. Securing flows and billing data :

Reduced risk of loss or fraud compared to paper format.

Modern electronic invoicing systems guarantee robust data protection thanks to advanced security protocols.

Security is a top priority, and your customer and practice data is protected by advanced encryption systems and security protocols, guaranteeing the confidentiality of sensitive information.

The dematerialization of supplier invoices provides greater security in the processing of information.

In addition, invoice and RIB fraud is a problem that more and more firms are beginning to face.

Electronic invoicing secures payments by certifying invoices with electronic signatures and stamps, protecting firms and their customers against fraudulent or erroneous invoices.

Your invoices will also be less contentious.

All dematerialized invoices will be stored in a secure, centralized and backed-up area.

All your documents are stored on secure servers hosted in France.

Billing software for lawyers ensures data security, protected by encryption and advanced security protocols.

The chosen solution must guarantee optimum data protection through robust encryption measures.

2. Reliable, long-term electronic archiving: guaranteeing the probative value of documents.

Electronic writing, electronic forms, electronic exchanges and digital copies are recognized as valid in law.

Digital tools and trust services are also recognized by legislators and case law, such as digital safes and electronic archiving.

For a dematerialized invoice to have the same force as a paper invoice, it must meet the criteria for retention until the end of its retention period.

This means guaranteeing the authenticity of the origin and integrity of the content.

Reliable, long-term electronic archiving is essential to guarantee the probative value of documents.

The use of appropriate software enables us to comply with the new requirements for computerized, tamper-proof accounting, and all invoices will be stored in a secure area.

3. Better visibility and traceability of transactions: Facilitate audits and internal control.

As far as traceability is concerned, electronic invoices offer precise tracking of transactions, which is essential for transparency and for responding to any requests or audits.

Traceability of any modifications is ensured by permanent, documented controls.

The use of software allows you to track customer payments , follow up invoices in real time to facilitate reminders, and keep precise track of transactions.

You can follow :

the status of your invoices,

track the number of emails opened by your customers,

and electronic invoices provide greater visibility and traceability of transactions.

Electronic invoice management facilitates data processing.

The transfer of financial information becomes almost immediate, and accounting management is more precise and responsive.

d) Improved image and customer relations.

Going paperless goes beyond the technical and financial aspects: it modernizes the firm's image and strengthens ties with customers.

1. Modernity and professionalism: Demonstrate your firm's ability to adapt to new challenges.

Dematerialization is part of the modernization of administrative practices, in line with the rise of legaltech.

The dematerialization of invoices is a strategic imperative for the complete digitization of a firm's activities.

Successfully making this transition is an advantage for remaining competitive in an increasingly digital legal environment.

The switch to electronic invoicing is often presented as a way of modernizing business relationships.

5) How do I manage dematerialized invoices?

The set-up is complete, and electronic invoices come and go. But how do you orchestrate this new flow on a daily basis?

Good management is the key to sustaining the benefits of dematerialization.

What reflexes and tools are needed for smooth, secure management?

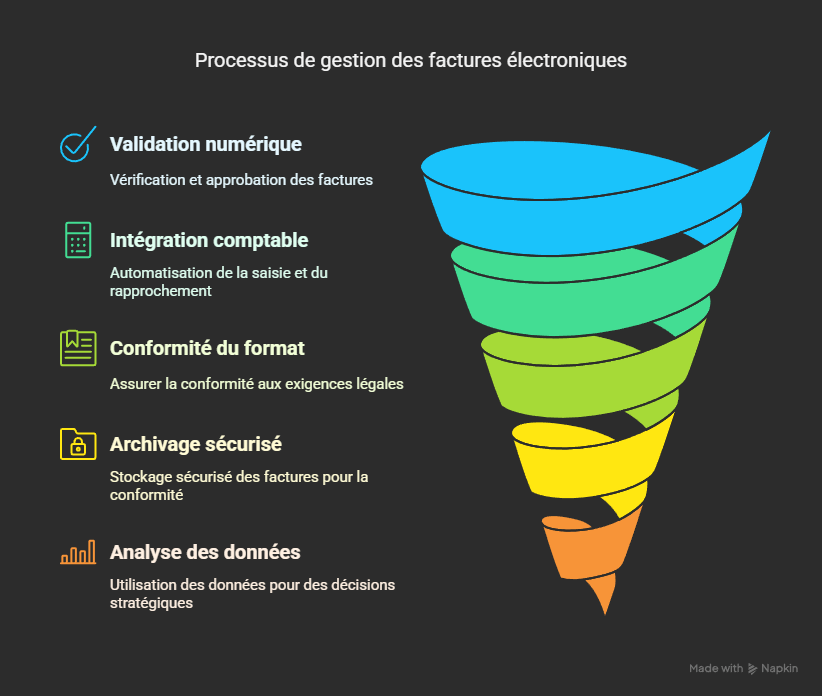

a) Organize the processing of incoming invoices.

Receiving invoices in electronic format requires a reorganization of processing workflows.

1. Set up a digital validation circuit: Who checks and approves the supplier invoice received?

EDM systems or dematerialization solutions analyze :

incoming invoices,

extract key information

and submit them for digital validation before accounting settlement.

Standardizing supplier invoice management is an advantage.

2. Integrate dematerialized invoices into your accounting system: Automate data entry and reconciliation.

Automated data entry and reconciliation facilitate accounting management, making it more precise and responsive.

Some software programs allow you to record payments received and track the balance in real time.

3. Manage different reception formats.

To be considered a dematerialized invoice within the meaning of the law, the entire process must be electronic, from issue to archiving.

An invoice that is initially on paper, then scanned and sent by email, is not an electronic invoice.

The tax authorities accept several technical formats, such as :

PDFs,

XML,

CSV,

JSON,

YML.

Structured formats (EDI, advanced electronic signature) are accepted, and functionalities may exist to convert a native PDF into a structured format or enable online data entry.

Sending PDF invoices by email is acceptable if the company ensures traceability and integrity, that the PDF comes from the invoicing software (not scanned), and with the customer's prior agreement.

b) Control the issue and follow-up process.

1. Ensure the conformity of each invoice issued: format, mandatory information, electronic signature if necessary.

Electronic writing, electronic formalities and electronic exchanges are recognized as valid in law.

Electronic invoices must contain all the mandatoryinformation required on a conventional paper invoice.

For a dematerialized invoice to have the same force as a paper invoice, it must :

authenticity criteria,

integrity

and legibility of its issue at the end of its retention period.

This can be guaranteed by a qualified electronic signature, EDI (Electronic Data Interchange), or documented and permanent controls to establish a reliable audit trail.

Billing software for lawyers ensures compliance with legal standards.

Invoice fraud can be reduced by certifying invoices with an electronic signature or stamp.

2. Optimize payment tracking: Use invoice status (issued, received, paid) and automate reminders.

Dematerialization facilitates accurate tracking of transactions and speeds up collection, improving cash flow management.

Billing software for lawyers makes it easy :

payment tracking,

automatic reminders,

and avoid late payments.

Automated dunning saves valuable time in tracking unpaid invoices.

3. Make it easier for customers to access their invoices (customer portal?).

Dematerialization facilitates exchanges with third parties.

Dematerialized invoices can be made available to corporate customers, enabling them to easily retrieve their invoices without having to call on the secretariat.

Some management tools include customer database management, enabling you to quickly view customer-related items, including paid and unpaid invoices.

c) Secure electronic archiving with probative value.

The electronic archiving of invoices is an obligation and an important issue.

1. Choose a compliant electronic archiving solution (digital safe, SAE).

You need to choose a billing solution that includes digital archiving to avoid legal or administrative complications.

Specific solutions exist for securing information storage, guaranteeing confidentiality and complying with retention conditions.

Digital archiving and storage are trusted solutions.

Invoices are stored in a secure, centralized location, limiting errors and facilitating reporting.

Modern systems ensure robust data protection thanks to advanced security protocols.

Tax-compliant dematerialization also means that archiving solutions must comply with current regulations.

Since 2000, the firm has been involved in electronic archiving law, and has published a book on the NF Z42-013 standard.

2. Define a clear archiving policy: who archives what, where and how?

Choosing the right solution means :

easily integrate and retrieve invoices,

store documents in a centralized tree structure,

and ensure their safety and accessibility.

d) Use data to manage the firm.

Beyond simple compliance, dematerialization enables data to be used for better management and strategic steering of the firm.

1. Use billing information to analyze profitability (file, customer, service).

Invoicing software allows you to track and invoice activities, helping you to better monitor profitability per case.

By defining rates and hourly volumes that can be parameterized according to the nature of the work or the person involved, the new software programs enable you to draw up :

coherent,

attractive

and profitable,

valuing each task in its own right.

Rapid access to customer and file information enables us to better manage relationships and respond to requests.

2. Monitor key indicators: average payment time, non-payment rate, sales in real time.

The use of invoicing software makes it possible to track payments and set up automatic reminders, thus reducing payment times and collection procedures.

Invoice status (issued, received, paid) is a useful indicator.

The tax authorities themselves will use the invoicing data collected in real time to enrich the programming of controls via data mining.

3. Make informed decisions thanks to accurate, automated reporting.

Centralized archiving systems facilitate reporting and data retrieval.

Precise transaction tracking and automated invoicing and processing provide up-to-date information for management purposes.

Modern management tools allow you to quickly visualize the key elements linked to a customer.

Data analysis is used to ensure that the volume of hours worked does not exceed the planned package.

6) What kind of billing software do you need?

Billing software is at the heart of modernizing your administrative practices.

a) The essential features of good lawyer software.

To make the right choice and avoid unpleasant surprises, certain criteria and features are essential:

Invoicing software that complies with the new regulations is essential.

It must be able to handle the required formats, such as Factur-X, which enables structured information from the software to be included in a PDF document.

The dematerialized invoice solution must be compatible with the tax authorities' "Y" transmission system, involving exchange via the public PPF platform or PDP-certified private platforms.

The software also needs to manage e-reporting, i.e. the transmission to the tax authorities of data relating to transactions not covered by e-invoicing.

PDP pre-registration, like Tiime (approval 0037), is an advantage in anticipating the reform.

Electronic invoicing should be automatic with certain software packages.

2. Fine-tuned fee management: time spent, fixed price, subscription, expenses and disbursements.

The legal profession uses a variety of billing methods:

time,

on a flat-rate basis,

or by subscription.

A good software package should enable you to manage and mix these different billing methods, as well as easily record and re-invoice expenses and disbursements.

The software must also allow different rates to be set according to the nature of the task or the person involved.

Precise management of time spent, even if it is no longer the only basis for invoicing, is still necessary to measure the profitability of projects.

3. Integration with case management and time tracking: a 360° view of the customer.

For optimized management, the billing tool must be integrated with file management and time tracking.

Some internal practice management software packages, such as Tempolia or Hub Avocat, include electronic invoicing and centralize customer information and documents.

This integration makes it possible to monitor profitability by file, and ensure that nothing is forgotten when invoicing.

An easy-to-use CRM to centralize contacts and exchanges is also a useful feature.

4. Module for tracking unpaid invoices and automated reminders.

Optimizing cash-flow management is one of the advantages of dematerializing invoices.

Good invoicing software should offer accurate payment tracking and a potentially automated reminder system to manage overdue payments and accelerate collections.

b) The different types of solutions on the market.

The market offers various solutions for billing lawyers:

1. All-in-one business software for lawyers: the promise of native integration.

Many software packages are specifically designed for law firms, integrating billing functionality alongside case management, time tracking and other aspects of the legal business.

These solutions, such as Axonaut (which bills itself as the best lawyer software ), Hub Avocat (with Invoicer), Tempolia or SECIB, are designed to meet the specific needs of the legal profession.

They often offer a simple, intuitive interface.

2. General-purpose billing software: Can they do the job? What are their limitations?

The use of non-adapted software or manual methods such as Word and Excel are presented as "old-fashioned" to leave behind, error-prone and less secure.

We can deduce from this that general-purpose software, if it does not offer specific functions such as :

time management by activity/provider,

folder integration,

fine-tuned management of disbursements,

compliance with professional secrecy,

specific Factur-X formats,

PPF/PDP connection), may not be sufficient or may require complex adaptations.

Companies will be able to use either the public portal directly, or a certified third-party dematerialization platform, which will route the invoices and communicate the data to the authorities.

4. The potential of customized solutions (No-Code/Low-Code): When standard isn't good enough.

Some firms may have very specific needs that are not fully covered by standard market solutions.

Developing bespoke tools or applications via a no-code agency with No-Code/Low-Code approaches could offer a high degree of flexibility and customization.

c) The selection process: How to avoid making a mistake?

Choosing the right software is a decisive step in ensuring a successful transition to electronic invoicing.

Given the diversity of solutions on the market, a methodical approach is required to select the tool best suited to your law firm's needs.

1. Define your precise needs and budget: the specifications.

The first step is to take stock of your existing organization and billing processes.

This includes an inventory of existing flows, processes, tools and data.

You need to assess how e-billing can be integrated with your existing tools to maintain business continuity.

An audit of dematerialization needs can be carried out.

This preliminary analysis makes it possible to define exactly which functionalities are essential, and to draw up specifications, often accompanied by an impact analysis.

2. Compare solutions: Ask for demonstrations, test interfaces.

Once the requirements have been defined, it's time to identify the e-billing platforms and software that comply with current regulations and are specialized for the needs of law firms.

Many solutions offer free demos to help you evaluate their features and interface.

Testing these tools (for example, by creating a few invoices, as suggested by Hub Avocat, or by taking advantage of trial offers) is the best way to compare the different offers and see how they apply to your own management.

3. Evaluate ergonomics and ease of use for your teams.

The adoption of new software depends largely on how easy it is for your entire team to use.

The interface must be intuitive and easy to use, even for lawyers who are not accounting experts.

A well-designed tool should automate time-consuming tasks and make invoice management quick and easy, enabling invoices to be generated with just a few clicks.

4. Check the quality of technical support and the solution's scalability.

The choice should not be limited to immediate functionalities.

It's important to ensure the reliability of the solution and the quality of the customer support offered.

Available, competent support teams can greatly simplify implementation and day-to-day use.

It is also important to check the software's ability to evolve with the needs of the firm and future regulations.

Some solutions are described as scalable, with frequent updates based on user feedback.

The ability to integrate with other applications (such as CRM or records management), as well as data security and confidentiality parameters - important for professional secrecy - are also important technical aspects to evaluate.

Finally, the ability to train your teams to use the new tools is a key success factor.

7) What are the deadlines for electronic invoicing?

a) The official and progressive reform timetable.

The reform of electronic invoicing, which aims to generalize the use of invoices in electronic form, has seen its timetable initially scheduled for 2024 postponed.

According to the new timetable set out in the Finance Act for 2024, this obligation will come into force gradually, for both receipt(e-invoicing) and data transmission(e-reporting).

1. September 1, 2026: All firms (subject to VAT) must receive electronic invoices.

From September 1, 2026, all VAT-registered businesses, regardless of size, will have to be able to receive invoices in electronic format.

This obligation applies to all taxable persons, including law firms.

2. September 1, 2026: mandatory e-invoicing and e-reporting for large companies and SMEs.

Also, from September 1, 2026, large and mid-sized companies will be required to issue invoices in electronic format (e-invoicing) and to transmit transaction data (e-reporting).

This dual obligation applies to transactions between VAT taxpayers.

3. September 1, 2027: mandatory e-invoicing and e-reporting for SMEs and VSEs (most law firms).

For small and medium-sized enterprises (SMEs), very small enterprises (VSEs) and microenterprises, the obligation to issue electronic invoices (e-invoicing) and transmit data (e-reporting) will come into force on September 1, 2027 .

The majority of law firms are affected by this key date for issuance, while at the same time being required to take delivery from September 1, 2026.

The initial timetable for e-invoicing called for general roll-out on January 1, 2026 or 2027, with intermediate stages from July 1, 2024 (universal reception and issuance for large companies).

b) Why anticipate now?

There are several reasons why it's a good idea to anticipate compliance.

1. Take the time to choose the right solution and the right support partner.

Switching to electronic invoicing requires the use of partner dematerialization platforms (PDP) or the public invoicing portal (PPF).

Choosing a solution that complies with current regulations and is adapted to the specific needs of law firms takes time.

Giving yourself enough time allows you to evaluate your options and select a reliable partner.

A successful transition involves checking that your tools are compliant and training your teams in the new processes.

Anticipation means taking stock of your organization, integrating e-invoicing into your existing tools to maintain operational continuity, and testing the chosen solutions.

The pilot phase allows you to practice exchanging invoices, and to guarantee data security and confidentiality.

This allows for gradual implementation, avoiding last-minute stress.